pic from Business Times

pic from Business TimesBefore the release of the Budget, many were wondering what can the government do to help the economy in the absence of external demand?

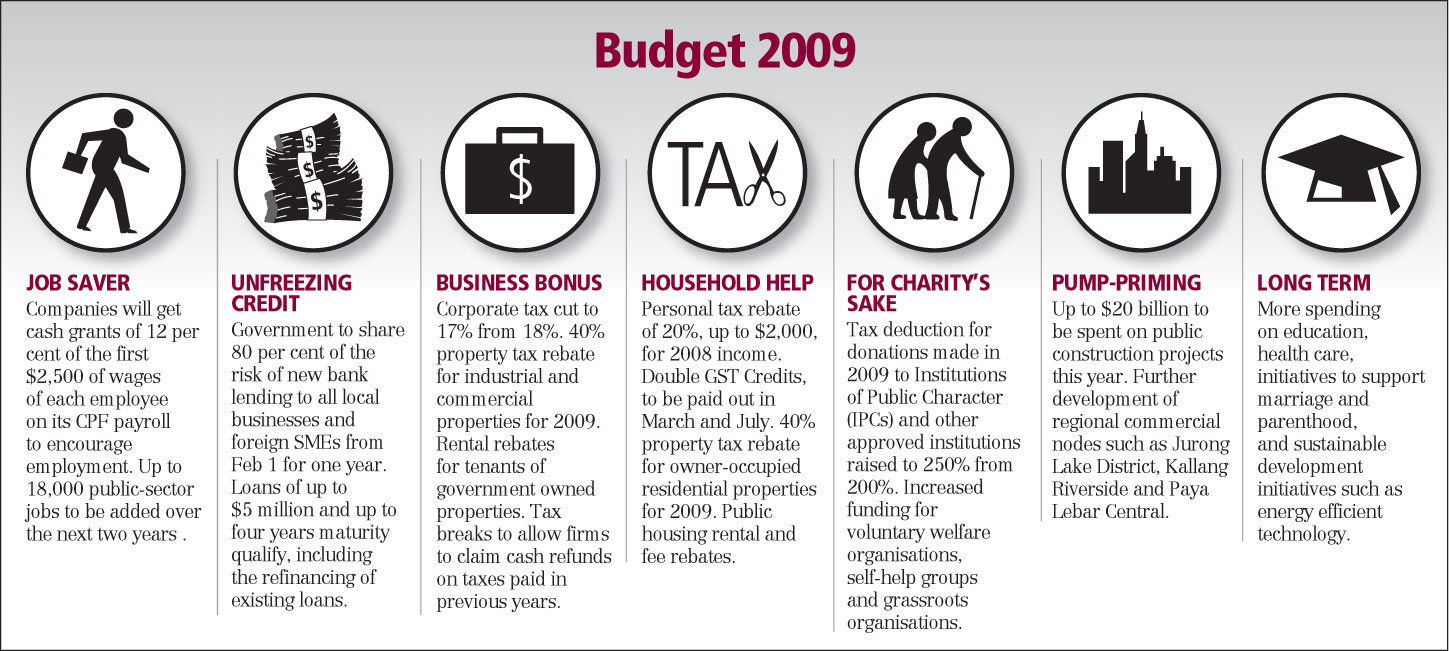

On Thursday 22 Jan 2009, the Budget presented looks like a modified version of the efforts to revive a war-ravaged economy of a country immediately after the world war.

At that time, there was obviously no external demand and many of the surviving population were unemployed and living in poverty. The government then used borrowed money (from World Bank I think) to pay labour and materials to build roads, bridges and our now famous HDB flats!!

In today‘s Singapore, we are planning to use part of our reserves to partially pay for all our salaries (Jobs Credit Scheme) and another $20billion for construction projects.

For the Jobs Credit Scheme, the government will give cash grants of 12% for the first $2,500 salary of a Singaporean employee. So if your gross salary is $1,800, your boss will get a refund of $216 per month from the government.

My immediate off-the-cuff response would be that all of us will be partially working for the Government ie. part-time civil servants!!

Based on YA 2007 figures, there were about 825,000 residents who reported income tax. Assuming 300,000 are non-Singaporeans, at $200 cash grant per person per month for about 500,000 Singaporeans, it is certainly no small sum.

Definitely a bold budget indeed.

P/S – Singapore Budget 2009 May I know the person who came up with “Jobs Credit Scheme” idea?